Workhorse Group Inc. (WKHS)

Is $WKHS Stable or Time to be Put to Pasture?

Workhorse Group Inc. (WKHS) is a MICRO-CAP company founded in 2007 and began public trading on the Nasdaq in January 2016. In their own words from Workhorse’s website:

“We build dependable logistics solutions for all types of work. Made with durable EV components and intuitive technical features, our trucks and drones are engineered to make every job smarter, safer, and more productive than before.” https://workhorse.com/

Clint's Take: (Disclosure: At the time of writing this profile (01/19/24) I own stock in Workhorse Group Inc.)

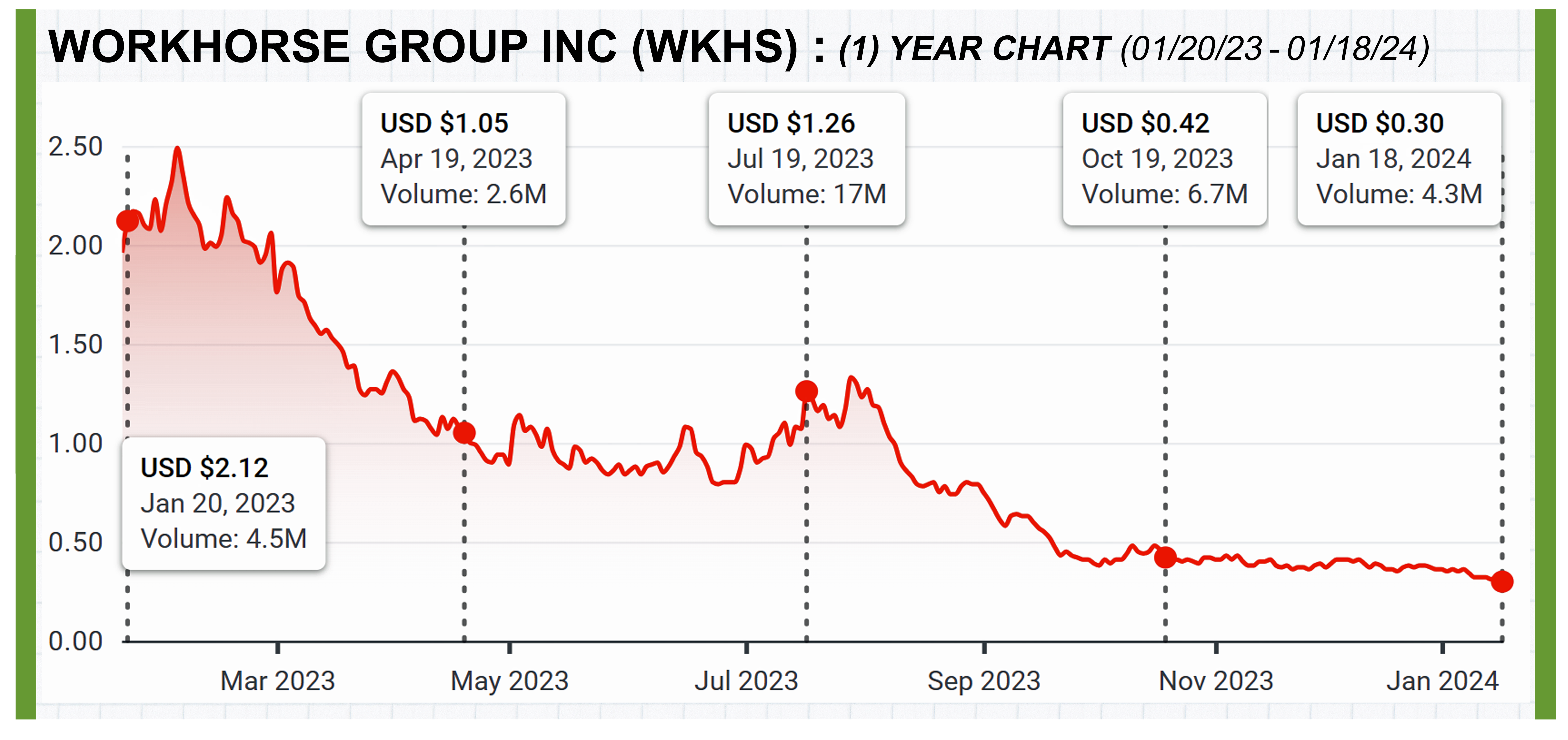

First, let me address the disclosure above. Workhorse Group Inc. (WKHS) has been on my books for a while now, and SPOILER ALERT: this post will not be an endorsement by me for anyone else to buy in now. Editorially speaking, WKHS was a candidate for the How Tuesday: Investing Resolutions for 2024, but we saved it for a complete profile. I had made some money with it but got greedy and went back to the trough. Despite marking a new 52-week low this past trading session, there were (and are) some parts of WKHS worth discussing more in-depth.

As I had said about the autonomous trucking company Aurora Innovation (AUR), the path to profitability will generally be in commercial application first. Personal use EV sales have seemingly stalled for car manufacturers, but a market still exists for businesses eager to move to cost-cutting green technologies. WKHS is one of those companies meant to fill that demand. WKHS hosts a complement of EV work and panel trucks (W4 CC, W750, and W56) with up to 150-mile ranges per charge. They also have two unmanned aerial systems (UAS), The WA4-100 Horsefly and WA4-200 Falcon, each with a 10lb payload and up to 45-minute flight capability (think drones for delivery). All their products are made in the US with EVs at the Workhorse Ranch in Indiana, capable of 10,000 trucks/year by 2025, and the UAS manufacturing in Mason, OH.

Early on, WKHS was criticized for spending too much time and capital on developing relationships with dealers before complete manufacturing was online. I disagreed with that assessment, which is why WKHS popped on my radar. A lot of EV start-ups showed a cool product video and spiked in pre-sale, then ultimately would have to backtrack and ended up failing to meet orders or expectations (i.e., Rivian (RIVN) and Lucid (LCID)). WKHS, in contrast, did not (wait for it…) put the cart before the horse (ahh, there it is). Their Certified Dealer Program now has eight dealers spread throughout the US who don't only offer sales but with certified technicians maintenance services after purchase. With a strong foothold in CA (Kingsburg Truck Center, Freeway Isuzu, and Fairway EV), news of receiving $85,000 voucher credits for the purchase of the W56 as part of the Hybrid and Zero-Emission Truck and Bus Voucher Incentive Project (HVIP) should show a boost for the dealers and WKHS alike.

From here, WKHS becomes a little streaky. Reports of UPS purchases (2018) and large orders beyond manufacturing capacity keep showing up in research for WKHS but little to follow up with. Barring any major news of a partnerships from delivery mainstays (outside of FedEx (FDX) in OH), the model seems stagnant. The "Stables by Workhorse" program offering charging for your fleet may be a step in the right direction for future growth. Just like we see in consumer EVs, charging availability is a significant obstacle to overcome, so there is that, but most of the numbers look paltry. Annual revenue is around $5M, and operating costs are nearer $97M for 2022. They have burned through cash on hand and used preferred stock sales (diluting value and having investors exit the position for the perfect storm) to try and bridge the gap. Reports of "fleet sales" equaling "15 vehicles" will not cut it to get back on track. The considerable economic borrowing costs for businesses may also have much to do with WKHS's lackluster sales. While I do like the company and the infrastructure it built, I don't like where it is right now, and it may take some time before it can get itself above water (just like my position in it).

Phil's Take:

On paper, I am a fan of electric vehicles in the freight space. In the time I have been writing this, delivery vehicles for Amazon (AMZN), UPS (UPS), and FedEx (FDX) have driven by my house, and my local postal service worker has also dropped off my mail. FDX spends roughly 6% of its revenue on fuel costs, up from 4.8% in 2016 and 5.6% in 2019. Reducing the cost of last-mile delivery will be a huge priority for the US economy in the future.

WKHS seems to be in a solid position to compete for market share. They have a strong product line, manufacturing capacity, and a growing list of certified dealers in their network. I also like that they have "Stables by Workhorse," and an actual FDX ground fleet in Cincinnati, Ohio, that they manage and are converting to an all-electric operation. It feels like an odd diversion for a manufacturing company, but having their actual product operating in real-world scenarios is a fantastic opportunity to demonstrate credibility and value to a potential customer base.

The question is whether WKHS can rebound in time. Their delay in getting the HVIP voucher certification set them back dramatically at a time when they were spending cash to ramp up production capacity. They have yet to recover market confidence. Each press announcement does little to bolster the stock price. The fate of the drone segment of the business is also a question that could drag down the share price unless sales grow.

I'm waiting to see if WKHS can get out of its own way. They are in a position to have the kind of year they were expecting when the stock traded in the $1 range back in July and August. But that's just hopeful speculation. WKHS has some innovation and a good network, but neither translates to a sound investment now, given the stock's last 3-month performance. (sorry, Clint). If delisting weren't a real threat (currently at sub $1), I would put WKHS on the watchlist and wait for the price to bottom out before re-evaluating. Yet waiting until March for their next earnings report and then hoping they can return to Nasdaq compliance (if necessary) is just too big of an ask right now.

Moving Forward:

We agree that now is not the time for WKHS, so we are putting it on the "Backburner" watchlist. There needs to be some fundamental changes for the company before we give it any future consideration. For example:

A considerable uptick in sales

A partnership with a major delivery company

Some traction in their UAS division

The stock price to return and sustain Feb/Mar 2023 levels

The March Q4FY23 earnings call may give some insight into future growth or a peek if there has been a slowdown of the “cash burn”. In the meantime, we will continue to listen for any news that may show it getting back on track and update accordingly.

Thanks for reading! We'd love to hear from you with any questions or comments you have to share in the discussion below.

You can get updates on Workhorse Group Inc. by subscribing for FREE today and check out the Ledger Island Watchlist for the complete list and latest looks on all the companies we cover in our weekly Spotlights.